Joe Leahy wrote . . . . . . . . .

Visiting Beijing late last year, the EU’s chief diplomat Josep Borrell complained that China’s trade surplus with Europe was soaring even as its market became tougher for European companies to enter.

“Either the Chinese economy opens more, or you may have a reaction from our side,” Borrell warned.

Last week, the response came. The EU wielded new anti-subsidy powers for the first time in a raid on the Warsaw and Rotterdam offices of Nuctech, a Chinese manufacturer of airport and port security scanners.

The raid, the latest in a series of trade-related investigations by the EU against Chinese companies, comes as China’s trading partners protest against what they argue is a flood of underpriced exports from the world’s second-largest economy. While Beijing incentivises investment in manufacturing, it does too little to spur household consumption, they charge.

China’s seeming reluctance to rebalance its economy is one of the great challenges facing global financial systems, threatening to worsen Beijing’s trade and diplomatic relations not only with western countries but also with developing nations.

Both inside and outside China, there is a strongly held view among many economists that the country could secure a further period of robust growth if it were able to boost consumption by its own citizens. Indeed, faced with a property crisis, President Xi Jinping has taken some one-off measures to stimulate consumption to offset a fall in domestic demand.

But Xi has eschewed more radical medicine, such as cash transfers to consumers or deeper economic reforms. His latest campaign is instead to unleash “new quality productive forces” — more investment in high-end manufacturing, such as EVs, green energy industries and AI.

According to analysts, the reasons for the lack of more radical action on consumption range from a need to generate growth quickly by pumping in state funds — this time into manufacturing — to the more deep-seated difficulties of reforming an economy that has become addicted to state-led investment.

Ideology and geopolitics also play roles. For Xi, China’s most powerful leader since Mao Zedong, the greater the control his country exerts over global supply chains, the more secure he feels, particularly as tensions rise with the US, analysts argue. This leads to an emphasis on investment, particularly in technology, rather than consumption.

Under Xi, security has also increasingly taken precedence over growth. Self-reliance in manufacturing under extreme circumstances, even armed conflict, is an important part of this, academics in Beijing say.

“China should be prepared for war,” says Liu Zhiqin, senior researcher at the Chongyang Institute for Financial Studies at Renmin University of China. “The conflicts in Europe and currently in the Middle East have repeatedly proven the importance of maintaining a robust manufacturing capacity and ample inventory.”

The pressure on Beijing to find a new growth model is becoming acute, analysts say. China has become too big to rely on its trading partners to absorb its excess production.

“The exit strategy has to be, at the end of the day, consumption — there’s no point producing all this stuff if no one’s going to buy it,” says Michael Pettis, a senior fellow at the Carnegie Endowment in Beijing.

Few projects capture Xi’s vision for 21st-century Chinese development as well as Xiongan, a new city being built on marshlands about 100km from Beijing.

At a lake in the “modern socialist prototype city”, the voice of Chinese opera singer Yin Xiumei singing “my motherland and I, never shall we part” blasts out from hidden speakers across the water while a system of intricate fountains simulates ballet dancers. The display is an example of how no expense has been spared to impress visitors to what Xi has called China’s “1,000-year project”.

Xiongan unites many of Xi’s favourite development themes. Through vast investment in mega-infrastructure projects such as a high-speed rail hub, Xiongan aims to bring state-owned enterprises, universities and entrepreneurs together to concentrate on high-technology innovation, from autonomous vehicles and life sciences to biomanufacturing and new materials. As of last year, about 1mn people were living there, $74bn had been invested and 140 companies had set up there, Beijing says.

Conspicuously absent from the city plans are strategies to encourage the thing China’s economy lacks most — domestic consumption. In guidelines released in 2019 for Xiongan by Xi’s cabinet, the State Council, there was no mention of the term “consumption”, except for “water consumption”.

Economists have called for years for China to do more to stimulate consumption to rebalance an economy that is overly dependent on debt-fuelled investment.

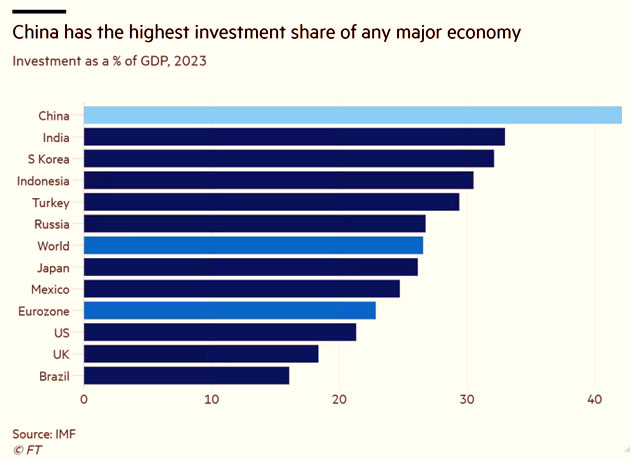

China’s investment to gross domestic product ratio, at more than 40 per cent last year, is one of the highest in the world, according to the IMF, while private consumption to GDP was about 39 per cent in 2023 compared to about 68 per cent in the US. With the property slowdown, more of this investment is pouring into manufacturing rather than household consumption, stimulating oversupply, western critics say.

“China is responsible for one-third of global production but one-tenth of global demand, so there’s a clear mismatch,” US secretary of state Antony Blinken said in Beijing last week.

China’s slower economic growth since 2021, which follows the bursting of the real estate bubble, has spawned numerous papers from domestic experts about the problem.

“Demand contraction is not new; it has persisted since the late 1990s,” Xu Gao, the chief economist at Bank of China International, said in a recent speech to the National School of Development (NSD), Peking University, which was distributed by the newsletter The East is Read.

Xu pointed to China’s high national savings rates, which, at more than 47 per cent of GDP in 2022, are double the world average, as one symptom of the problem.

The reasons Chinese people save so much range from a lack of good investment options, especially with property in the doldrums, to inadequate social welfare and healthcare. The IMF calculates China spends 8 per cent of GDP on social protection schemes, slightly more than the US but half that of Japan. While Xi has declared China’s ambition to build “a great modern socialist country”, he has said it must not “fall into the trap of ‘welfarism’ that encourages laziness”.

“The objective of economic growth is to fulfil the people’s expectation for a better life,” Xu said, adding this should be manifested through “enhanced consumption — better quality food, clothing and leisure activities”.

China’s premier Li Qiang, Xi’s number two official, in his annual work report in the rubber stamp parliament in March, listed numerous schemes to encourage people to spend. They included incentives to upgrade home appliances and buy electric vehicles, and efforts to improve elderly and childcare and other services.

The report’s main emphasis was on Xi’s “new quality productive forces”. Since Xi first touted the term in September last year, 1,073 articles about the idea have appeared in China’s largest academic database CNKI, according to Jean Christopher Mittelstaedt at the University of Oxford. In Li’s report, while the terms “consumption” received a combined 11 mentions the words “investment”, “manufacturing” and “industrial” or “industrialisation” appeared a collective 69 times.

Economists suspect that behind the rhetoric, the investment in manufacturing is partly pragmatic. With the property market still falling three years after the crisis began, and many indebted provinces ordered to suspend large infrastructure projects, Xi needs to find growth somewhere to meet his 5 per cent target for this year.

“The bottom line is they want growth in output and they want the jobs associated with that growth,” says Stephen Roach, a faculty member at Yale and former chair of Morgan Stanley Asia. He says when “they’re clamping down on property, it doesn’t leave them with much choice but to go for a production-oriented growth stimulus”.

This was the pattern in previous slumps, such as after the 2008 global financial crisis and a slowdown in 2015-16, says Pettis of the Carnegie Endowment.

“The solution has always been a massive increase in investment,” Pettis says. But, he adds, with signs of over-investment now “everywhere”, from the property sector to overbuilt infrastructure, and debt to GDP at about 300 per cent, “you can see that investment can no longer be the solution”.

China’s responses to criticism from the west about manufacturing overcapacity have become increasingly shrill.

“Washington’s recent rhetoric has morphed into yet another Sinophobic catchphrase,” state news agency Xinhua said in a commentary in April. Chinese officials argue that charges of overcapacity are just another ruse from the US to contain its development.

China’s current account surplus is well below historical highs, at 1.6 per cent of GDP in the first three quarters of 2023, according to the IMF.

But western businesspeople say the imbalances are bigger than the headline figures would suggest. China is sending about four containers to Europe for every one full of goods that returns, says Jens Eskelund, president of the European Union Chamber of Commerce in China. “We’re seeing overcapacity across the board,” he says.

In a report, “Overcapacity at the Gate”, the Rhodium Group said that since Covid struck in 2020 China had been supporting industrial companies with a stimulus programme through tax credits, subsidies and interest rate cuts, in order “to keep struggling companies afloat and workers employed”.

“When economic growth continued to disappoint in 2023, Beijing’s policy support kept the emphasis on producers, as their bias against ‘welfarism’ kept policymakers from stimulating consumption,” the research group said.

The report found that in early 2023, China’s industrial capacity utilisation rate fell below 75 per cent for the first time since 2016 while inventories have increased and 20 per cent of companies are lossmaking.

“I think part of it is ideological,” says Camille Boullenois, co-author of the report, of the preference for manufacturing and investment. “There’s also this very deeply rooted idea of this trickle-down economy — that companies provide employment and you should be supporting them rather than individuals, who are by their nature untrustworthy.”

China’s systematic efforts to build up self-reliance from foreign technology have also spurred its heavy investments in production and technology, a report from the EU Chamber showed.

The drive for self-sufficiency started in the mid-2000s, long before Donald Trump, as US president, began his trade war. China’s reliance on global supply chains for inputs into its products has decreased in line with this strategy.

In 2014, Xi introduced the concept of “comprehensive national security” encompassing multiple aspects of the economy and society, according to the EU Chamber report.

“This has been going on for at least about 8-10 years,” says Zhiwu Chen, chair professor of finance at the University of Hong Kong, of China’s shift to an industrial policy that takes into account “war preparation”.

In an article in Qiushi, the Communist party journal, in 2020 during the depths of Covid, Xi wrote that China needed to expand domestic consumption and achieve a balance between supply and demand.

But China also should “develop technologies that will give us a decisive advantage” and . . . deepen China’s involvement in global industrial chains. By doing so, we will develop an effective deterrent against attempts by other countries to sever our supply chains,” he said.

In areas vital to China’s national security, the country needed supply chains that “are self-sufficient at critical moments”, he said. “This will ensure the economy functions normally in extreme circumstances.”

HKU’s Chen says China no longer measures its “national power” in purely economic terms “but more importantly, in terms of military . . . capacity. And this is why manufacturing is very important”.

He says in this vision of the world, consumption is a lower priority.

The challenge of China’s investment-driven model, however, is how much longer it can work. While the party claims to be achieving its real GDP targets, with growth reaching 5.2 per cent last year, in nominal terms it grew 4.2 per cent as prices weakened.

Less pricing power means less investment in the long run, analysts say.

The Rhodium Group argues that some of the loans that flowed into the industrial sector last year went to local government finance vehicles, the heavily indebted off-balance sheet investment holding companies of provinces and municipalities.

While large sums still went to manufacturers, they “do not have a strong appetite to expand capacity given falling prices”, Rhodium said in a report.

Economists say that for consumers to feel comfortable to spend more, particularly after the property slump, China needs to step up its development of social welfare programmes and healthcare. While China has made strides in building out its public pension and healthcare systems, they are still lacking.

But such solutions would take a long time to boost consumer confidence and would require massive new funding from government coffers that are running dry.

Greater consumption would also necessarily mean reducing the role of manufacturing or investment in the economy. This could be done by unwinding China’s intricate system of subsidies to producers, which includes government infrastructure investment, access to cheap labour, land and other credit, says Pettis.

But if that was done in a big bang fashion, the share of household consumption to GDP would increase while overall GDP would contract as manufacturers suffered. This was obviously not a politically preferable option for Xi.

“They are locked into this system,” Pettis says.

Some argue that one way China could rebalance the economy would be to distribute trillions of dollars of shares in state-owned assets and companies to its citizens.

In an article last year, also distributed by the newsletter The East is Read, Bank of China International’s Xu recommended creating multiple state-owned investment funds to hold the state enterprise equity. These funds’ shares could then be distributed evenly among all citizens.

Economists say that while Xi might be reluctant to dilute central government assets, it might be more politically acceptable to redistribute holdings held by China’s local governments, some of which are asset-rich. One of China’s most indebted provinces, Guizhou, for instance, owns the country’s premier liquor company, Moutai.

While the debate about a new growth model continues, the risk is that excess investment in manufacturing could worsen deflationary pressures in the country, discouraging private investors and ultimately leading growth to grind lower. This would hurt not only China’s but global growth.

“If the response just continues to be a supply-side reaction to a demand-side problem, then it’s going to be pretty tricky,” says Thomas Gatley, senior analyst at Gavekal Dragonomics. “Particularly as we’ve already seen, the response to [China’s growing exports] from both developed markets and indeed increasingly emerging markets is getting a bit more pugnacious.”

Source : FT